Hello Everyone,

Here is a link to the March Newsletter.

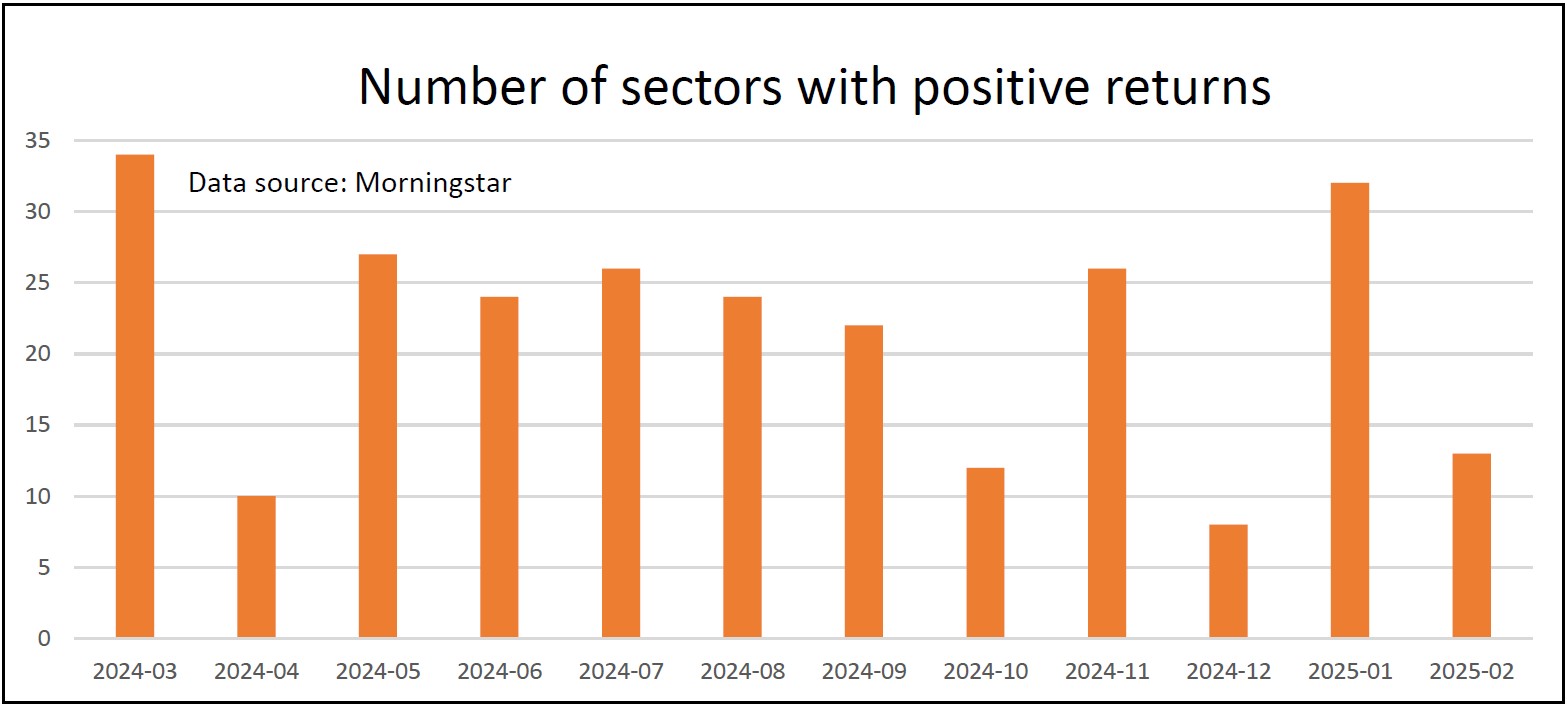

Out of the 34 Investment Association sectors that we track each week, only 13 went up in February.

That was an improvement on the eight that went up in December, but a significant drop from the 32 that made gains in January.

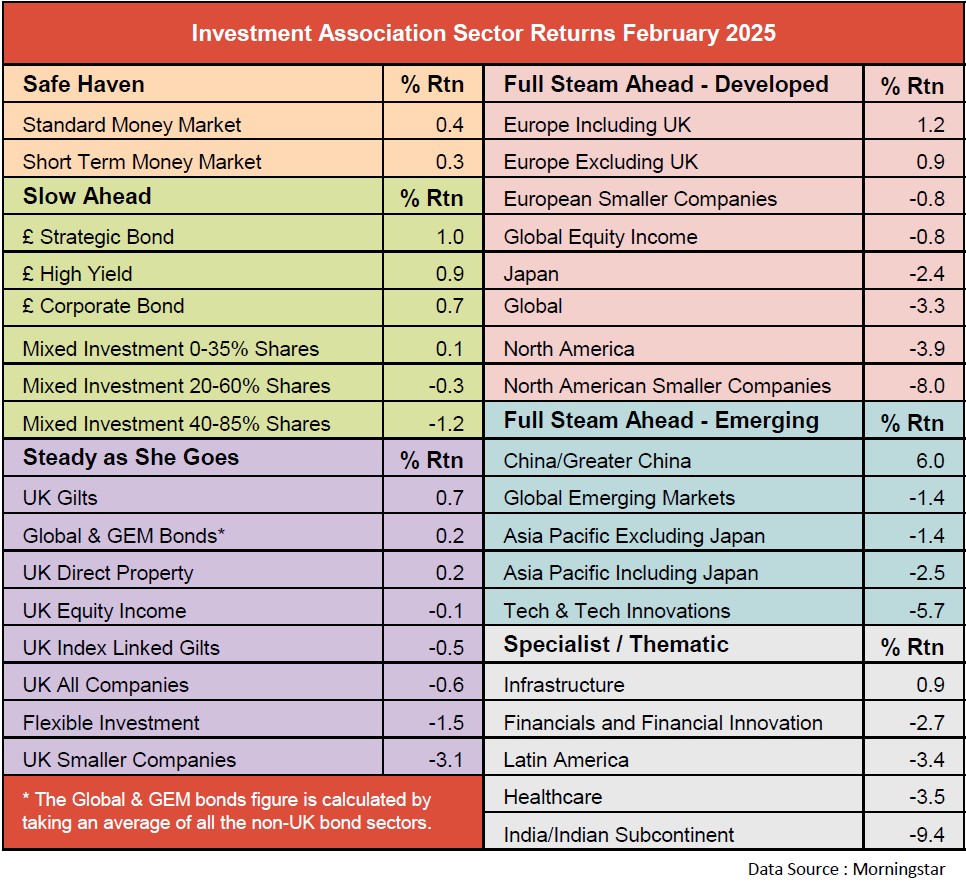

As you would expect, the two Money Markets sectors made further gains last month, and most of the sectors investing in bonds also went up. However, the sectors investing in equities did not perform as well.

The China/Greater China sector rose by 6.0%, but the UK equity, American, Japanese, Asia Pacific, and Global sectors all went down, as did most of the thematic sectors. However, the Europe including UK and Europe excluding UK sectors did post gains in February.

Only four equity-based sectors have risen in both January and February. Over the two months, the Europe excluding UK sector leads the way with an 8.6% return, followed closely by the Europe including UK sector, which has made 8.5%. Then it’s the China/Greater China sector, up 7.3%, and finally, the Infrastructure sector, with a two-month return of 2.1%.

Unfortunately, in the first two weeks of March most sectors have seen further losses.

The sectors that were performing well this time last month have all taken a turn for the worse, especially the North American and Technology sectors.

This has meant that both demonstration portfolios have struggled in recent weeks.

We have made more changes than normal over the last month, switching out of the funds that we are holding that have gone down into some of our longer term holdings that continue to make gains.

In the Ocean Liner we have also selected a couple of funds that have been performing particularly well in recent weeks – Baring German Growth and Baillie Gifford China.

As always, I hope that you enjoy this month’s newsletter, and I look forward to hearing any feedback.

Out of the 34 Investment Association sectors that we track each week, only 13 went up in February.

That was an improvement on the eight that went up in December, but a significant drop from the 32 that made gains in January.

As you would expect, the two Money Markets sectors made further gains last month, and most of the sectors investing in bonds also went up. However, the sectors investing in equities did not perform as well.

The China/Greater China sector rose by 6.0%, but the UK equity, American, Japanese, Asia Pacific, and Global sectors all went down, as did most of the thematic sectors. However, the Europe including UK and Europe excluding UK sectors did post gains in February.

Only four equity-based sectors have risen in both January and February. Over the two months, the Europe excluding UK sector leads the way with an 8.6% return, followed closely by the Europe including UK sector, which has made 8.5%. Then it’s the China/Greater China sector, up 7.3%, and finally, the Infrastructure sector, with a two-month return of 2.1%.

Unfortunately, in the first two weeks of March most sectors have seen further losses.

The sectors that were performing well this time last month have all taken a turn for the worse, especially the North American and Technology sectors.

This has meant that both demonstration portfolios have struggled in recent weeks.

We have made more changes than normal over the last month, switching out of the funds that we are holding that have gone down into some of our longer term holdings that continue to make gains.

In the Ocean Liner we have also selected a couple of funds that have been performing particularly well in recent weeks – Baring German Growth and Baillie Gifford China.

As always, I hope that you enjoy this month’s newsletter, and I look forward to hearing any feedback.

Kind regards and best wishes,

Richard Webb

Managing Director

Comments

0 comments

Please sign in to leave a comment.